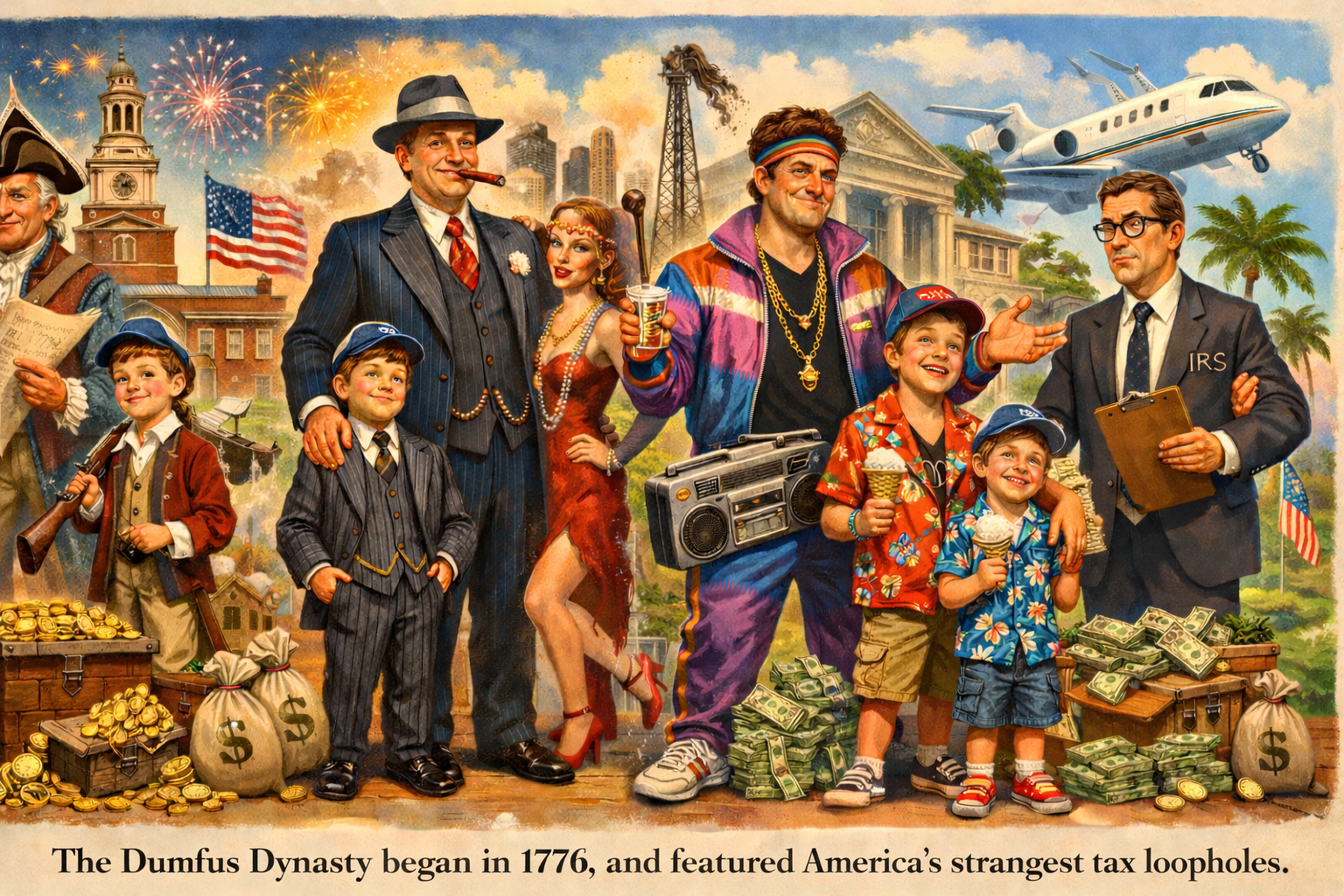

My name is Dakota Donald Dumfus.

That has been the name of every male member of my family for the past nine generations, which has caused confusion for historians, genealogists, creditors, prosecutors, and the Internal Revenue Service.

If you read the financial pages—or the criminal pages—you may have heard of us.

Historians call us The Dumfus Dynasty. The IRS calls us “a continuing administrative situation.”

The Beginning

The dynasty began in 1776, when my ancestor Dakota Donald Dumfus opened an accounting office in Philadelphia.

Some historians claim the American Revolution had already begun, but family records strongly suggest the conflict accelerated shortly after Dakota Donald Dumfus filed his first tax return.

His client was a cobbler who owed the British Crown three pounds in tax but possessed only two pounds and a goat.

Dakota Donald Dumfus studied the situation, tapped the goat thoughtfully, and declared:

“The goat is clearly a business expense.”

At that moment the American accounting profession was born, although for several decades decent citizens still regarded it as a borderline occult activity.

The Family Rules

The Dumfus family followed three sacred principles:

- Always balance the books.

- Never waste a deduction.

- Always name the child Dakota Donald Dumfus.

Especially the third rule.

Most wealthy families build dynasties with railroads, factories, or oil wells. The Dumfus family built ours with something more reliable: a deductivorous accountant.

The secret to multiplying a fortune is surprisingly simple:

Hire a deductivorous accountant.

Then keep him out of jail.

A deductivorous man, in case you’re unfamiliar with the species, feeds on deductions the way wolves devour sheep.

He does not merely locate deductions. He stalks them. He corners them. He drags them screaming from the dark corners of the tax code.

A truly deductivorous accountant can discover a tax advantage hiding in a garden shed, a church raffle, or a sandwich consumed within sight of a ledger.

The Great Dumfus Methods

Over the centuries the Dumfus family refined accounting into something between science, theater, and organized misdirection.

The first great breakthrough was the Dumfus Reversible Goat Principle, developed immediately after the cobbler incident.

Under this rule any livestock involved in a business transaction could be classified simultaneously as inventory, transportation, equipment, lawn maintenance, and morale support.

If the goat later ate the records, that merely proved it was part of the filing system.

Later generations expanded this reasoning to mules, chickens, and one deeply unreliable donkey in Maryland that was depreciated for eleven straight years.

Then came the celebrated Phantom Expense Doctrine.

This doctrine held that any expense which would have existed under slightly different circumstances deserved financial recognition.

Under Phantom Expense accounting one might deduct:

- meals that should have been eaten,

- trips that almost happened,

- wages that would have been paid if competent employees had existed,

- rent for offices wisely never leased.

Critics called this fictional accounting. The Dumfus family preferred the phrase “pre-realized financial truth.”

But the real masterpiece was Deferred Birth Accounting.

This began when a Dumfus child was born so close to midnight on New Year’s Eve that six witnesses recorded six different birth times.

To ordinary families this would have been a story.

To the Dumfus family it was a tax strategy.

If a birth could be treated as a floating accounting event, then age itself became flexible.

A Dumfus heir could be:

- seven years old for inheritance law,

- twenty-eight for investment eligibility.

If he had been born one day earlier—or one day later—the math changed entirely. Especially around February 28th.

He could end up seven. Or twenty-eight.

The family called this Chronological Optimization.

The Treasury Department called it something else, usually while shouting.

The Naming System

No Dumfus innovation, however, proved more useful than naming every male heir Dakota Donald Dumfus.

This created extraordinary legal advantages.

When a summons arrived, the family could truthfully say: “Dakota Donald Dumfus is no longer available.”

Which was correct.

He had either:

- retired,

- died,

- moved upstairs,

- or become a different Dakota Donald Dumfus.

Authorities eventually discovered that pursuing a Dumfus ended up as:

The Ledger Fog Defense

Whenever investigators grew suspicious, the Dumfus family deployed the Ledger Fog Defense.

This involved presenting auditors with towering ledgers, perfect cross-indexes, and columns so beautifully balanced they induced professional admiration.

The numbers were flawless.

The only difficulty was that no one could determine what they described.

One Treasury investigator reportedly closed the final ledger and muttered:

“The numbers balance perfectly. I simply have no idea what they are balancing.”

He retired the following Tuesday.

The Present Generation

And now the responsibility falls to me, Dakota Donald Dumfus IX.

I inherited the ledgers, the portraits, three cabinets of incomprehensible documents, and the family reputation—less a reputation than a very long rumor.

The Dumfus dynasty has survived revolutions, depressions, banking reforms, income tax, war tax, electronic filing, and forensic accountants who believed numbers should correspond to reality.

Through it all we have remained what we have always been:

patient, prosperous, numerically elegant, and faintly indictable.

The Final Audit

Recently an IRS auditor named Milton Cray announced he had finally cracked the Dumfus system.

He arrived with documents, charts, and a color-coded family tree the size of a pool table.

After two hours of explanation he pointed triumphantly at me.

“I have you now, Dakota Donald Dumfus.”

I nodded politely.

Then my father entered the room.

He was Dakota Donald Dumfus.

Then my son entered.

He was Dakota Donald Dumfus.

Then my grandfather was wheeled in from the terrace.

He was also Dakota Donald Dumfus.

The auditor stared at the four identical signatures on the table.

Finally he whispered, “Which one of you filed this return?”

Our lawyer smiled gently and replied:

“That depends entirely, sir, on which Dakota Donald Dumfus you mean.”

The auditor studied the signatures again and sighed.

Then he asked the question that has defeated the Treasury Department for 240 years:

“Which Dakota Donald Dumfus do I arrest?”